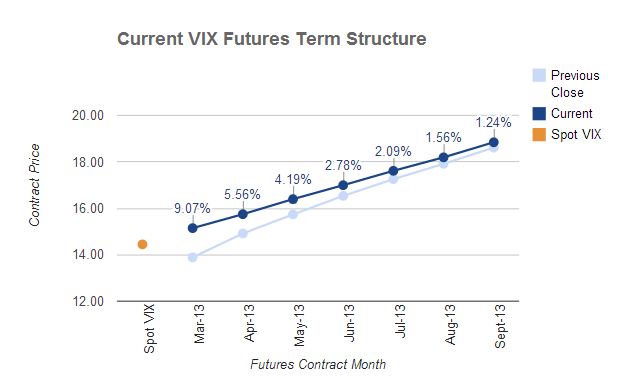

The VIX futures curve flattened notably today, with front month futures closing just 0.65 below second month futures and the difference between 1st month and 7th month compressed to just 3.7 points. This flattening often indicates that there is imminent downside in the broader market and could move VXX higher and XIV lower (although I don't like long being VXX without backwardation in first two months).

Term structure as of close today:

Coinciding with these technical signals, the market expressed its displeasure of the FOMC when they suggested that they may need to reduce the $85Billion of QE that goes into the market each month, citing that continued QE may prompt excessive risk and that the economy is on a moderate growth path. But whether the level of QE can actually be reduced without causing an equity market sell off and a costly rise in interest rates remains to be seen.