Regardless of the "news events" that pundits say are driving the market, the reality of this market is that the FOMC's attempts to reflate an asset bubble by artificially suppressing interest rates through quantitative easing has forced everyone to chase returns in the stock market using heavy leverage. With ongoing issues of Japan's deflationary problems, Europe's insolvency and unemployment problems, and the U.S.'s deficit problem that no one is truly interested in solving, sooner or later the market will gets a dose of reality when evidence resurfaces to show once more that natural economic growth cycles, which include both growth and recession, cannot be suspended forever. When that happens it is only natural to see some selling.

While front month VIX futures closed in a very slight backwardation today I am not rushing to buy VXX here. Over the past three days VIX has made an oversized move has risen 29.4% compared to the S&P 500's -1.85% so I will be looking to buy XIV if the market can find some support in the next couple of days. However with front month VIX only at 17.65 there is no assurance that shorting VIX is a good play just yet. After hitting market highs after 7 straight weeks up we're likely to see choppy trading and an increase in realized volatility as traders look protect profits and perhaps try to unwind some positions.

A couple things to watch out for 1) Bernanke's semiannual testimony on the Monetary Policy Report starts tomorrow at 10:00am ET. A hawkish tone or a hint that QE is at it's useful limits could cause a bearish reaction similar to last Wednesday's selling after the FOMC minutes, and 2) The huge move in the Yen today is likely to crush Japan's stock market tomorrow and may shake investor confidence globally. Should bad news continue and the backwardation spread of M1 and M2 increase I will be long VXX.

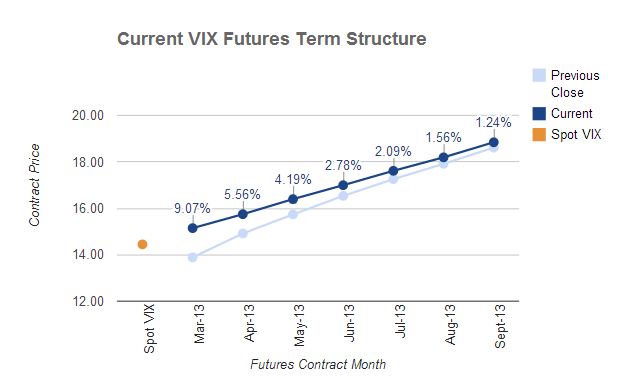

A look at today's monster move across VIX futures: