Has the S&P 500's longest bull market in history, with its 336% gain, finally converted you to become a part of the buy-and-hold equity herd?

Do you think the U.S. equity market is now immune from the carnage we've seen recently in Emerging Markets (MSCI Emerging Market Index is now off 20% from the January highs)? Have you cast aside the idea of a balanced investment portfolio?

You probably don't want to even think about it, but this bull market will not last forever.1 There will be an equity bear market here in the U.S. Non-diversified investors risk facing losses similar to that of the 2000 dot com bust and the 2008 financial crisis. The trap is that we don't know when. Any perma-bears left are still taking on losses, ineptly sitting in cash, or getting crushed by cryptocurrencies.

I personally like an aggressive Modern Portfolio Theory portfolio with a heavy weighting on equities -- but with one important modification. I like to carve out a small portion of my portfolio and allocate it to process-driven volatility trading which is long volatility at times and short volatility at other times.

This is the concept of including volatility as an asset and there are right and wrong ways to do it.

- Wrong way #1: Buy-and hold a short volatility ETP.

XIV, which was the short volatility ETP of choice, suffered a catastrophic hit in February 2018 and investors lost hundreds of millions of dollars. Prior to going bust, XIV was the "can't lose" fund that returned over 10x since inception in 2010. Many people lost nearly all of their investment and various professional money managers were fired because they didn't know what they were doing and ignored the trouble signs of the underlying assets (VIX Futures). The calamity was so bad, that some brokers banned the purchase of short volatility ETPs to try to protect the average investor (a bit late for that, don't you think??).

- Wrong way #2: Buy-and-hold a long volatility ETP.

If buy-and-hold of the short side of volatility is wrong, then it must be better to buy-and-hold long volatility ETPs, such as VXX? No. VXX and the 2x leveraged UVXY & TVIX ETPs suffer long term decay thanks largely due to the fact that these funds track VIX Futures that are most often in a state of contango. Without getting technical, it should be sufficient to point out that VXX has gone from over $100,000 (adjusted for multiple reverse splits) to $27 over the course of its lifespan since inception 9 years ago.

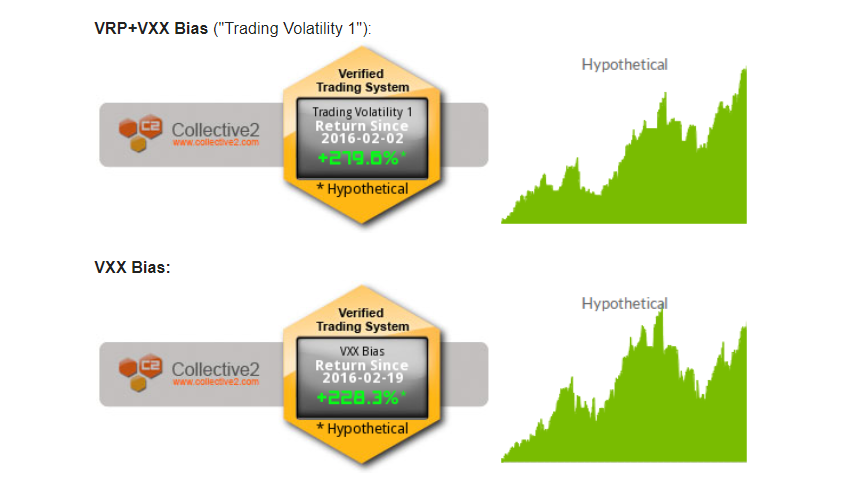

- The Right Way #1: Our VRP+VXX Bias indicators.

Our volatility indicators put us in cash, long volatility, or short volatility based on daily measurements of various components within the volatility market in order to provides us with a "flexible" fifth asset (the others being equities, bonds, real estate, and commodities). To take diversification one step further, our volatility trading indicators are comprised of multiple unrelated component indicators. No single indicator is perfect and ours are no exception. When they don't agree on what to do we move our volatility allocation to cash (this by the way, is how we survived the February volatility market imploded).

One really nice aspect of our VRP+VXX Bias algorithms, in addition to being fully automated, is that they get us invested in an asset that is non-correlated with other assets. This is key to good diversification within a portfolio. Why? Because if you are diversifying using an asset that has high correlation to another invested asset, you are diversifying in name only while both assets carry roughly the same performance.

The flip side of the non-correlated asset coin, however, is the fact that there will be times when our indicators lag the market. 2018 has been pitiful so far and this can be frustrating if you are not looking at the big picture. And that is, a properly diversified and properly balanced portfolio will excel long term.

At any given time there will be a lagging asset within a diversified portfolio. Smart investors don't just scrap an asset class after a bad month/year -- they rebalance and focus on their process knowing that the next year is likely to result in an entirely different outcome. Otherwise, the investor is left with a portfolio that carries less diversification, greater risk, and a lower long-term return potential.

Our indicator's performance speaks for itself with actual automated signals and trades tracked by a third party since 2016, Collective2, here:

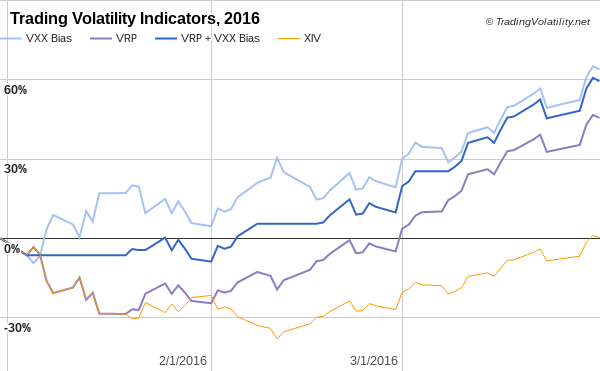

Looking further back using our modeling, we can see how VRP+VXX Bias ("Trading Volatility 1" performs in a variety of market conditions. By far, the best performing years for our indicators are when strong equity drawdowns occur, as can be seen in the chart below.

Trading Volatility+ subscribers have access to our VRP and VXX Bias indicators, our intraday indicator data, receive emails with preliminary and final change alerts for each of the indicators as well as our daily summaries, and interact with our private community of volatility traders in the forum. If interested, you can learn more about our services on our Subscribe page.

As always, each day's indicator values, buy/sell triggers, trade performance summary, and equity curves are tracked in the spreadsheets linked at the bottom of our Subscribe page. Additional information on our trading strategy and indicators can be found on our Strategy page.

Our indicators are also utilized by a volatility investment fund that is open only to accredited investors. If you think a managed volatility fund might better fit your needs please send a message through the Contact page.

Footnotes:

1 Smart people like to pretend they know why this bull market will end: the end of fiscal stimulus, rising interest rates, inflation, deflation, stagflation, global recession contagion, too much debt, high P/E ratios, trade wars, etc. No one knows the why or when and the average investor is unlikely to guess the when, and how it plays out, and be able to invest appropriately.

------------

Hypothetical and Simulated Performance Disclaimer

The results are based on simulated or hypothetical performance results that have certain inherent limitations. Unlike the results shown in an actual performance record, these results do not represent actual trading. Also, because these trades have not actually been executed, these results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity. Simulated or hypothetical trading programs in general are also subject to the fact that they are designed with the benefit of hindsight. No representation is being made that any account will or is likely to achieve profits or losses similar to these being shown. Hypothetical and backtest results do not account for any costs associated with trade commissions or subscription costs. Additional performance differences in backtests arise from the methodology of using the 4:00pm ET closing values for SVXY, VXX, and ZIV as approximated trade prices for indicators that require VIX and VIX futures to settle at 4:15pm ET